Dan Reiter, CFP®, CPA®

Many retirees assume healthcare costs become more predictable once they enroll in Medicare. But for higher-income retirees, Medicare premiums can fluctuate based on income decisions made years earlier.

A Roth conversion, large capital gain, investment sale, or even higher retirement account withdrawals can unexpectedly increase Medicare premiums through a surcharge known as IRMAA. And because Medicare looks back at prior-year income, many people do not realize the impact until after retirement decisions have already been made.

Think of IRMAA as a requirement for higher-income individuals to pay a larger share of their Medicare costs rather than having those costs subsidized by the federal government.

The federal government pays up to 75% of Medicare Part B and Part D premium costs for most beneficiaries. However, that subsidy gradually decreases at higher income levels. For those in the highest income brackets, the government subsidy can fall to as little as 15%.

According to the 2025 Annual Report from the Board of Trustees that oversees Medicare, 5.1 million Medicare Part B beneficiaries paid higher premiums due to their income. Moreover, the number of beneficiaries impacted is projected to increase by more than 40% to 7.2 million by 2030. Total IRMAA premiums paid by Part B beneficiaries alone exceeded $14 billion in 2025 and are projected to increase to more than $28 billion by 2030.

As more retirees become subject to IRMAA, planning for healthcare costs and taxes becomes an increasingly important part of a sound retirement income plan. Many are surprised by additional Medicare costs only after receiving a premium increase letter. However, proactive tax and retirement income planning to reduce or manage these costs is possible

uNDERSTANDIng HOW IRMAA IS CALCULATED

IRMAA is calculated based upon two variables:

- One’s tax filing status for the year, and

- Their modified adjusted gross income for two years prior to the premium year.

Tax filing status is the filing status on your tax return.

Taxpayers that file a joint tax return with a spouse are granted higher income thresholds before IRMAA charges kick in. All other taxpayers are subject to lower income thresholds. Other taxpayers include those that file as single, head of household, married filing separately, or as a qualifying surviving spouse with a dependent child.

Modified adjusted gross income (MAGI) for Medicare and IRMAA is defined as the beneficiary’s adjusted gross income (found on line 11 of the tax return) plus any tax-exempt interest income received (line 2a of the tax return).

It is important to note that only income that is reported on the tax return and subject to tax is used in the IRMAA calculation. The only exception is tax-exempt interest income, such as those from municipal (state and local) bonds. More on specific income sources and how those impact IRMAA and Medicare premiums later.

Each year, the Centers for Medicare & Medicaid Services (CMS) sets a baseline standard premium for Part B based on expected plan costs for the year per beneficiary. Then, the federal government subsidizes between 15% and 75% of the total cost depending on your modified adjusted gross income.

In 2026, Medicare Part B IRMAA amounts are calculated as follows:

|

2024 MAGI (Married Filing Joint) |

2024 MAGI (All Other Taxpayers) |

Government Subsidy Percentage |

IRMAA Monthly Surcharge (per beneficiary) |

Part B Total Monthly Premium (including IRMAA) Per Beneficiary |

|

< $218,001 |

< $109,001 |

75% |

$0 |

$202.90 |

|

$218,001 - $274,000 |

$109,001 - $137,000 |

65% |

$81.20 |

$284.10 |

|

$274,001 - $342,000 |

$137,001 - $171,000 |

50% |

$202.90 |

$405.80 |

|

$342,001 - $410,000 |

$171,001 - $205,000 |

35% |

$324.60 |

$527.50 |

|

$410,001 - $749,999 |

$205,001 - $499,999 |

20% |

$446.30 |

$649.20 |

|

>$749,999 |

>$499,999 |

15% |

$487.00 |

$689.90

|

Medicare Part D (prescription drug) coverage operates slightly differently. Part D plans are sold and administered by private insurance companies for which the base premiums may slightly vary. In 2026, Medicare Part D (prescription drug) IRMAA amounts are calculated as follows:

|

2024 MAGI (Married Filing Joint) |

2024 MAGI (All Other Taxpayers) |

Government Subsidy Percentage |

IRMAA Monthly Surcharge (per beneficiary) |

|

< $218,001 |

< $109,001 |

75% |

$0 |

|

$218,001 - $274,000 |

$109,001 - $137,000 |

65% |

$14.50 |

|

$274,001 - $342,000 |

$137,001 - $171,000 |

50% |

$37.50 |

|

$342,001 - $410,000 |

$171,001 - $205,000 |

35% |

$60.40 |

|

$410,001 - $749,999 |

$205,001 - $499,999 |

20% |

$83.30 |

|

>$749,999 |

>$499,999 |

15% |

$91.00 |

In early fall (October-November) the Social Security Administration pulls tax return information to calculate new Medicare premiums and any applicable IRMAA adjustments for the upcoming January 1st change. As many returns have not yet been finalized due to extension deadlines, they must use the tax information from the year prior. For example, 2026 premiums (set in Fall of 2025) are set based upon the 2024 tax return and income information.

One could easily take note of the inherent unfairness in this two-year “lookback” rule. It is not uncommon for someone to retire on or after age 65, resulting in their modified adjusted income decreasing. Income could also decrease because of events such as death or divorce. In these cases, you can file a form with Social Security (SSA-44) requesting that premiums be calculated based upon the more recent tax year, or your anticipated income in the year ahead. Note, though, that it is not enough for your income to simply decrease. It must also be accompanied by a “qualifying life event."

What Retirement Income Can Trigger Higher Medicare Premiums?

Many common retirement income sources may result in an unexpected increase in Medicare premiums. It is important to understand first what modified adjusted gross income is, and what sources will have an impact.

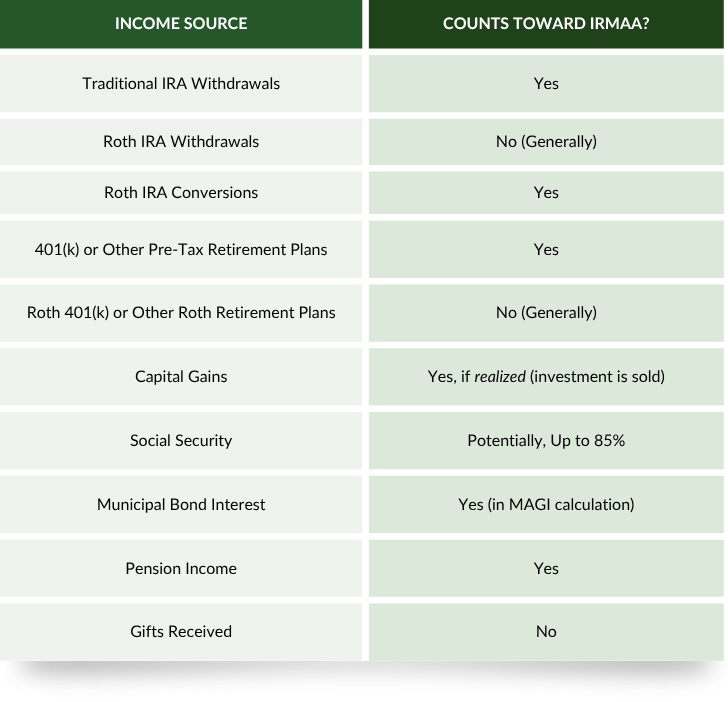

First, apart from tax-exempt interest, only income sources that are reported on the tax return and subject to tax are included in the calculation for modified adjusted gross income.

Non-Taxable Income Sources

Some income sources are not taxable. For instance, qualified distributions from a Roth IRA or Roth workplace retirement plan are not subject to tax. As such, distributions from these accounts are not generally included in the calculation for IRMAA. Similar rules apply to personal gifts received from friends and family, as well as alimony or maintenance pursuant to a divorce that occurred after 2018.

As noted, the only exception to this rule is interest received from municipal bonds. Although exempted from income tax, these amounts are specifically added back to calculate MAGI.

Pre-Tax Retirement Accounts

Distributions from pre-tax retirement accounts such as Traditional IRAs or workplace plans such as 401(k)s are taxed on a dollar-for-dollar basis. As such, every dollar distributed from these plans will be included in the calculation of modified adjusted gross income.

Roth conversions are also included in income and will impact IRMAA. Roth conversions are where you can elect to “convert” all or a portion of your pre-tax retirement account to a Roth.

Pensions

Receiving pension income will generally be included in the IRMAA calculation, as it is subject to taxation. The only exception to this is for pensions that are not taxable, such as certain pensions resulting from disability.

Social Security

Social Security is included in modified adjusted gross income for IRMAA to the extent it is subject to income tax. The taxability of Social Security has its own rules tied to the amount of other income sources. Generally, however, for those that are in the income ranges where IRMAA is a concern, 85% of the Social Security benefits received are taxable and impact IRMAA.

Non-Retirement Brokerage Accounts, Dividends, Interest, and Capital Gains

Non-retirement accounts get a bit trickier. Unlike pre-tax retirement accounts where distributions from the account are subject to taxation on a dollar-for-dollar basis, distributions from non-retirement accounts are not subject to tax. Non-retirement accounts are accounts that are not generally created or funded through a workplace plan or have any special tax treatments. These include cash accounts or traditional brokerage accounts.

Income sources in these accounts will most commonly include interest, dividends, and capital gains.

Interest and dividends are included in MAGI in the year they are received, regardless of whether they are distributed from the account.

Let’s say you own a share of Microsoft. If Microsoft pays a dividend, that will be included in your income. However, let’s say that your Microsoft stock also increases in value by 8% during the year. This appreciation is called an unrealized capital gain. Unrealized capital gains are not included in income and thus have no impact on IRMAA. If you were to sell your share of Microsoft, however, you have now realized that capital gain and must include it in income.

A Summary of Income Sources and IRMAA Impact

Planning Ahead: How Roth Conversions and Other Tax Planning Strategies Can Reduce IRMAA

IRMAA and higher Medicare premiums may feel unavoidable, but there are several proactive tax planning strategies that can be utilized to minimize or reduce bad outcomes.

Although there are numerous strategies that may be employed to manage income in retirement, the five strategies discussed below are common for managing taxes (and IRMAA) in retirement:

- Creating tax diversification.

- A planned strategy for retirement income and withdrawals.

- Taking advantage of lower income “gap” years.

- Carefully considering when to begin taking Social Security benefits.

- Proactive Roth conversions.

The Benefits of Tax Diversity

One of the most significant questions for retirees is how they will replace their income from working after they retire. Said in a different way, one of the first decisions you will make in retirement is what account(s) you will pull money from to cover expenses.

Tax diversity is when you have options between different types of accounts where taking money out will have a variety of impacts. As discussed above, for example, withdrawing funds from a Roth account is most often done without tax consequence. Withdrawing funds from a pre-tax retirement plan such as a 401(k) or IRA will be taxed dollar-for-dollar, and taking money out of a non-retirement account will have a tax impact depending on how much appreciation the account has experienced. Finally, spending down cash has no tax impact. In order of worst to best impact on IRMAA, it goes: (1) pre-tax accounts, (2) non-retirement accounts (with gains), and (3) cash and/or Roth accounts.

Admittedly, creating significant tax diversity through savings must occur for years before retirement begins. If you are about to retire in one year, save $30,000 per year, and have contributed to nothing but your pre-tax 401(k) – you probably don’t have a lot of time or ability to diversify. However, if you’re fortunate enough to be reading this several years before retirement, you should be wary of entering retirement with nothing but pre-tax dollars.

A Planned Strategy for Withdrawals

If you are one of those fortunate enough (or received good advice) to enter retirement with tax diversification, it is imperative that you create a strategic and planned strategy for your retirement income.

Designing a retirement income and withdrawal strategy is one that is best done over several years. Hopefully, you do so with a good professional that takes a long-term view. Designing your income strategy should be done with many factors in mind. Such factors include your total expense needs, breakdown of account types, charitable goals, and Social Security timing – just to name a few.

A well-crafted withdrawal strategy for retirement income has significant implications on Medicare premiums and IRMAA.

To illustrate, consider the following example:

A Retirement Case Study - Stan and Jenny JonesStan and Jenny both retired December 31st of the previous year after turning 65 and enrolling in Medicare. They have accumulated about $3.6 million in retirement assets, which is made up of about $2.6 million in a pre-tax 401(k), $350,000 in Roth IRAs, $400,000 in a non-retirement account with substantial gains, and $250,000 in savings accounts. In the first year of retirement, they believe they will need $180,000 (about $15,000/month) to cover normal living expenses, $60,000 to replace a vehicle, and an additional $30,000 for a celebratory retirement trip to Europe. They have no other income sources and have not yet started Social Security. |

Lower-Income “Gap” Years

Another strategy to potentially limit IRMAA and additional Medicare premiums is to take advantage of lower income “gap” years.

What are lower income “gap” years? These are the years in retirement before taxable income is expected to increase. For instance, taxable income will increase for many retirees in the future because of starting Social Security or required minimum distributions starting. Required minimum distributions are the age you are required to withdraw a certain minimum balance from your pre-tax accounts – for most, either age 73 or 75.

Those that retire before age 63 may have an even more opportunistic gap. Why? Because income reported on your taxes more than two years prior to Medicare doesn’t have an impact on Medicare premiums!

A Word of CautionIndividuals that retire before Medicare must also have a plan for health insurance coverage. For some, enrolling in a health plan through the Health Insurance Marketplace® may be an effective option. Enrollment on the Marketplace® may also come with substantial assistance in the form of premium tax credits. If this is the case, special care should be given to how much income you realize and report on your tax return. These premium tax credits may be worth substantially more than Medicare premiums that might be saved later. |

How can you “take advantage” of certain gap years? You can do so by intentionally raising your income today to reduce it in the future. This can occur by intentionally withdrawing more money from pre-tax accounts to cover living needs, or by completing Roth conversions. Roth conversions are discussed in greater detail below.

When to Begin Taking Social Security

Deciding when to begin taking Social Security benefits is a weighty decision in retirement for many reasons. One of the more significant cons to beginning Social Security earlier, however, is tax efficiency. In our experience, this is also one variable that often goes ignored.

As discussed already, there often exists an opportunistic window of time in early retirement before Social Security and required minimum distributions begin. Obviously, then, starting Social Security earlier will impact that window of time by introducing a (potentially) taxable income source. In 2026 if you are single and have income above $34,000, up to 85% of your Social Security benefits may be subject to income tax. Married tax filers who earn more than $44,000 may have up to 85% of their benefit taxed.

You may not be faulted by thinking Social Security is more tax efficient than withdrawals from a pre-tax account or a Roth conversion since a portion of the Social Security benefit is not taxable. However, this ignores the long-term ramifications of taking less dollars from your pre-tax accounts today. Dollars left in pre-tax accounts today may also serve to increase required minimum distributions in the future.

Roth Conversions

Roth conversions are when you intentionally move money from your pre-tax retirement account (such as an IRA) into a Roth account. The net effect of this transfer of funds is to convert the dollars from pre-tax to Roth.

Why would you want to intentionally pay more in taxes today? To (hopefully) save more on taxes on Medicare premiums in the future!

As already discussed, Roth conversions may be utilized to accelerate income into the lower income “gap” years in early retirement or before staring Social Security. Shifting the income earlier has two potential effects: (1) reducing your future required minimum distributions (and income), and (2) increasing the amount of tax diversity to allow for more strategic distribution planning. Both of these effects are strategies discussed above.

Finally, converting to Roth is also a “freezing” strategy. It’s a “freezing” strategy because it eliminates taxable income on any future growth of the account. This is typically the most powerful benefit of doing a conversion. For example, let’s say a 60-year-old has $100,000 in a pre-tax IRA. At an 8% growth rate, this IRA will grow to over $466,000 by age 80. That’s $466,000 that will be taxed in the future, including the $366,000 in growth. If a Roth conversion of the $100,000 was completed, however, growth on the $366,000 is eliminated. Finally, for the 80-year-old, the required minimum distribution is over $23,000 less.

what to remember about irmaa

-

IRMAA is based on your tax filing status and modified adjusted gross income (MAGI) from two years before your Medicare premium year.

Most taxable income reported on your tax return is included in the IRMAA calculation. Tax-exempt interest is also factored into the calculation.

Depending on your income level, IRMAA can increase Medicare Part B and Part D premiums by thousands of dollars per year.

Tax diversification, lower-income "gap" years before Medicare, strategic Social Security timing, and tax-efficient withdrawal planning may help reduce or avoid IRMAA.

Retirement planning involves a lot of moving pieces, and Medicare premiums are one area that often catches people off guard. Decisions around withdrawals, Roth conversions, investment income, and taxes can all have an impact on what you ultimately pay for healthcare in retirement.

The good news is that with a little planning ahead, there are often opportunities to create more flexibility and avoid unnecessary surprises later.

If you’re approaching retirement and want to better understand how IRMAA may impact your overall financial plan, our team of CFP® professionals would be happy to help you explore your options and think through the decisions ahead. Schedule a meeting with us to get started.

Ready to Discuss Your Retirement Plan?

Schedule a conversation with one of our CFP® professionals.

Disclosures:

Case Study: Through the basic inputs, we gather general information about a hypothetical scenario and roughly estimate how that scenario may perform over time. The results presented are not intended to be recommendations of any investment, investment strategy, or account type, and are not based on your personal situation. Prosperity Planning is neither an attorney nor an accountant, and no portion of the content should be interpreted as legal, accounting or tax advice. Be sure to consult with a tax professional before implementing any investment strategy. Investment advice, financial planning, and retirement plan services are provided by Prosperity Planning, Inc., an SEC registered investment advisor. The information contained herein, including but not limited to research, market valuations, calculations, estimates and other material obtained from these sources are believed to be reliable. However, Prosperity Planning, Inc. does not warrant its accuracy or completeness. The information contained herein has been prepared solely for informational purposes and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or to participate in any trading strategy. If an offer of securities is made, it will be under a definitive investment management agreement prepared on behalf of Prosperity which contains material information not contained herein and which supersedes this information in its entirety. Any investment involves significant risk, including a complete loss of capital and conflicts of interest. The applicable definitive investment management agreement and Form ADV Part 2A will contain a more thorough discussion of risk and conflict, which should be carefully reviewed before making any investment decision.